Good news, renters, plus a dollop of bad.

The typical monthly rent in March was $1,910 per month, up 1.8% from a year ago. That represents the slowest rate of growth in rental costs since December 2020, according to a new Zillow study.

“Rents surged after the pandemic due to a sharp increase in demand colliding with limited supply and strong fiscal support,” Zillow senior economist Kara Ng told CBS News in an email. “Growth is now slowing as new supply comes online, demand normalizes and affordability constraints reduce landlords’ pricing power.”

In another boost for some renters, people’s income rose faster in March than rental costs, giving people a bit more financial wiggle room.

According to the online real estate marketplace’s findings, single-family rents rose 2.5% on an annual basis in March, the slowest rate Zillow has recorded since 2015, when it started collecting the data. Zillow defines single-family homes as attached or semi-attached row houses, duplexes, quadruplexes and townhomes. Multifamily home rents were $1,757 in March, up 1.3% from a year ago.

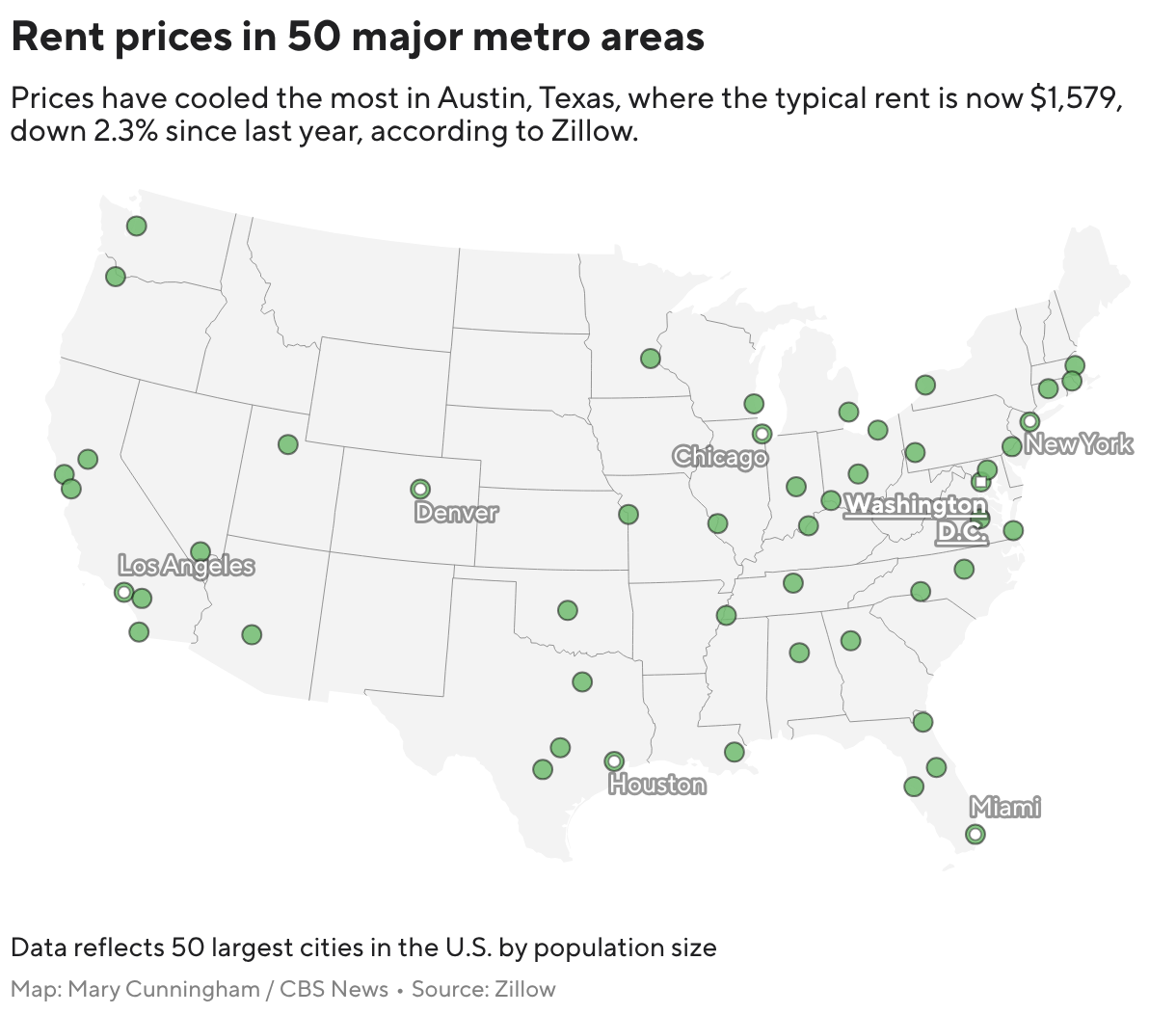

Among the largest U.S. cities, monthly rents cooled the most in Austin, Texas, where prices are down 2.3% as of March compared to a year ago. Rents are down 1.6% year over year in both Tampa, Florida, and San Antonio, Texas, Zillow found.

While the cost of keeping a roof over your head is cooling, Americans still spend a large chunk of their income on rent. The median household spent 26.5% of its income on rent last month, Zillow found.

Meanwhile, a household must earn at least $76,400 a year to comfortably afford the typical monthly rent of $1,910 — that’s up 35% from before the pandemic. The data shows single-family rents have surged nearly 45% since early 2020, while multifamily rents have jumped 28% over that period.